[Published on Yourstory.com]

India’s enterprise software industry has been slowly bubbling since the 1980s but has generally failed to deliver a large number of high impact, high value companies. We do have some companies that everybody talks about – iFlex, Tally, Zoho – but these are far and few between. I believe that we are seeing a new scalable wave of enterprise software companies coming out of India and there is a potential to deliver several high impact companies over the next decade. Here at Lightspeed Venture Partners, leveraging our global strength in enterprise technologies, we see opportunities to partner with companies that are cloud-native and have cracked a global market – examples of current active categories in India are CRM, analytics/big data, marketing automation and infrastructure.

India’s enterprise software industry has to be looked at separately from the outsourcing/BPO firms like Genpact, Cognizant, Tata Consulting Services and Infosys. Starting in the 1980s and early 1990s, this services industry is now mature and at scale.

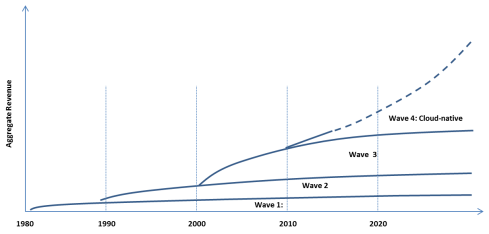

Separate from the outsourcing/BPO industry, India’s enterprise software industry (or “products” as it is called by many here in India) has evolved from the 1980s to now in what I think can be divided into four waves, coinciding somewhat with three trends: 1) enterprise software moving from desktop to client-server to cloud; 2) evolution of Indian industry post 1991 liberalization; and 3) increased experience of Indians at successful US product companies.

WAVE 1

The first wave of software products came along in the late 1980s/early 1990s – the focus was desktop products for business accounting. Companies in this wave include Tally Solutions (still the undisputed leader in SME accounting software in India), Instaplan, Muneemji and Easy Accounting.

WAVE 2

![]()

![]()

This generation of software products emerged in the 1990s as projects within outsourcing firms or from internal services arms of larger corporates. Infosys launched Finacle. Ramco Systems launched its ERP. And Citibank launched CITIL which became i-Flex. Other notable companies included 3i Infotech, Cranes Software, Kale Consultants, Newgen Software, Polaris Financial Technologies, Srishti Software and Subex.

I remember attending CEBIT in Hanover in 1989 when many of these Indian software and consulting companies were first introduced to Europe.

Did you know? Year 1989, the first time CeBIT introduced the concept of a partner country. Our first partner? India! pic.twitter.com/9sWx68Yzmp

— CeBIT India (@cebitindia) February 13, 2014

The late 1990s saw a wavelet of ASP (application service provider) startups in India, most of which got crushed after the dotcom bust.

WAVE 3

![]()

![]()

![]()

The 2000s saw on-premise India-first companies such as Drishti-Soft, Eka Software, Employwise, iCreate Software, iViz, Manthan Systems, Quick Heal Technologies, Talisma (for which I did some initial product management work while at Aditi Technologies) and Zycus get started. This was the era of 8-10% GDP growth in India which lasted till about 2010. Many of these companies had a direct sales model. After India, they generally expanded into the global South (Africa, Middle East, SE Asia, Latin America) where they found similar customer requirements and little competition from Western software companies. Bootstrapped in their earlier years, some of these companies grew over several years and have broken through to $25 million+ in annual revenue. Key verticals have traditionally been BFSI (banking, financial services and insurance), telecom, retail/FMCG (fast-moving consumer goods aka CPG in the US) and outsourcing/BPO.

Having been around for over a decade, some of these companies generally face the challenge of migrating to the cloud, upgrading user experience to modern Web 2.0 levels, and expanding addressable markets beyond the global South to the US and Europe. We have seen some of these companies get venture funded, typically at much later stages in their go-to-market relative to US-based software companies. Several of these companies have received funding in the past couple of years, ostensibly to “go international” and “go cloud,” not an easy task, especially when done together.

WAVE 4

Starting in around 2010, a new wave of cloud-native companies were launched, perhaps following the slowdown in India’s economy and the growth/acceptance of SaaS as a delivery model and as a sales model in the US. These companies have grown and now could power beyond the $10M/year revenue glass ceiling. The reason for the scale potential being higher for this cloud-native wave is the cracking of efficient online sales channels to reach markets globally.

Why this decade? Because there is an increased willingness of companies around the world to search for and buy software products online. There is now a large pool of founders who have worked at global enterprise product companies (e.g. Indian offshore development centers or in Silicon Valley itself with companies like SAP, Oracle, Google, Microsoft, Adobe) and have experience in product management, marketing and sales. And finally, there has been a dramatic reduction in the capital required to bootstrap enterprise software companies. Everybody uses AWS and software from other startups to get started. It’s quite meta.

Wave 4 companies have the opportunity to break through the barriers that previously relegated Indian enterprise software companies to selling to the global South. We have seen Atlassian (Australia), Zendesk (Denmark) and Outbrain (Israel) do this move to Western or global markets. Zoho is an Indian company that is rumored to be at $100 million per year revenue scale – they have been part of many of the waves I have described.

This cloud-native wave, I believe, can be divided into two dimensions. One dimension is the platform/tools companies versus workflow automation (applications) companies. The other dimension is India-first companies versus the global-first companies. We see opportunities in all four quadrants, each having its own challenges. We are interested in looking at companies in all these segments, with a bias toward companies which have reached some scale ($1M ARR) and are going after large addressable markets with aggressive sales & marketing execution.

| Applications | Markets: Enterprise (retail, banking, telecom, BPO, ecommerce) Examples: Capillary, Peel Works, Wooqer, Sapience Categories: Employee productivity, verticalized ————————————————— |

Markets: SMB/mid-market Examples: Framebench, Freshdesk, Kayako, MindTickle, Unmetric, Zoho Categories: Mature SaaS segments eg CRM, SMM, horizontal ————————————————— |

| Platforms/ Tools | Markets: IT dept, developers, SMB, media Examples: Exotel, Knowlarity, Germinait Categories: Telecom infra, app dev tools ————————————————— |

Markets: IT dept, developers Examples: Browserstack, FusionCharts, Little Eye, Mobstac, Webengage, Wingify Categories: app dev tools, marketing automation, security ————————————————— |

| Model: License+AMC, direct sales, resellers | Subscription, telesales, online sales (SEO/SEM,content mktg) | |

| India-first | Global-first |

[Please note this is not a comprehensive list of companies nor a view on which companies we admire or not]

Global-first companies coming out of India have started to crack or have cracked the online sales model, using SEO, SEM, content marketing and telesales. They are typically going after mature segments where buyers are typing keywords into Google at a high rate. This online selling model results in an SMB and mid-market customer base. In many cases, founders may have to move to the US to pursue direct enterprise sales. It’s worth noting that scale markets are not necessarily all in the US – companies could get built with a general global diffusion of customers, perhaps with help from resellers.

I see India-first companies typically going after newer high-growth companies in India (e.g. ecommerce, retail) and startups. Some go after Indian arms of multinationals (MNCs). This is a reasonable early adopter market to cut a product’s teeth on, but has limited ability to scale. Of the newer crop of India-first companies, very few go after large enterprises in India – there are exceptions like Peelworks and Wooqer. The model here generally is SaaS as a delivery model but not SaaS as a sales model (ie direct sales, not self-service). Many software companies are essentially verticalized.

We continue to see a few high-ticket, high touch direct sales enterprise software companies which are global-first, including companies like Cloudbyte, Druva, Indix, Sirion Labs and Vaultize. Many of these start out with teams in both Silicon Valley and India or transplant themselves to the Valley over time. I think this will continue to happen but we will not see the explosion here that we are seeing in the number of companies utilizing low touch online sales models. I see several high-impact companies coming out of these direct sales enterprise software startups as well.

I think this dichotomy between India-first and global-first companies is interesting and makes India a distinctly different type of investment geography, different from Israel (which has very small domestic market where tech companies move to the US very quickly), different from China (which mostly has domestic market focused startups and very little enterprise software) and different from the US (which is primarily domestic-focused in $500B enterprise tech industry in the early years of most startups). In terms of investor and founder interest, the pendulum may also swing back and forth between these two models as the Indian economy grows, sometimes at high speed, sometimes at a snails pace.

[With input from the team at iSPIRT and several of the companies mentioned above].

8 comments

Comments feed for this article

June 6, 2014 at 7:55 am

Sharat Chandra

In Wave4 also whether it is India First or the Global First approach, the interesting pattern to see is that for further sustained growth everyone is moving towards making US as the market and India as their outsourced product development center. This is the common pattern in all the examples shared above 😦 . Whats the point in this if the end purpose is to make India an outsourced product dev center 😛

June 8, 2014 at 10:43 pm

Dev Khare (@dkhare)

Fair point. There’s also a related phenomenon (small scale for now) where one could see smaller acqui-hires in India as being outsourcing 2.0.

Notwithstanding the impression the article may create, I think that the vast preponderance of enterprise/SMB product companies in India are targeting the Indian market and by extension other global South markets like ME, Africa, SE Asia, LatAm etc. I think this model is a valid model overall as a way to create a sustainable, profitable businesses. There are VC investors in India who have taken this model and invested behind it seriously.

However (and this my admittedly biased venture capital perspective), the longer gestation timelines (10-20 years historically) and smaller aggregate market sizes render this model somewhat tougher to invest in for venture investors like us. There are exceptions even here where one can squint hard and see a future where the growth trajectories can increase dramatically, perhaps with capital, perhaps with adding additional markets like the US/EU, perhaps with a more efficient demand gen/sales model.

June 4, 2014 at 11:01 am

This Fourth Wave of Indian Enterprise Software Startups is World-Class | ProductNation - The industry watering hole for software product industry. An iSPIRT initiative

[…] Reblogged from YourStory & LightSpeed Venture Partners blog. […]

June 1, 2014 at 10:37 pm

Jamie Edwards (@jmedwards)

Extremely insightful when putting things into perspective like that. Great post!

June 11, 2014 at 3:46 am

Dev Khare (@dkhare)

Thanks, Jamie. Where would you put Kayako in this mix?

May 30, 2014 at 8:25 pm

Dev Khare (@dkhare)

Thanks, Arpit. Will go look at those, have already met many that you mentioned. There are many many other companies that belong in each of these categories and the names I’ve mentioned are by no means a comprehensive list.

May 30, 2014 at 4:50 pm

Arpit

Great list, Dev. I think you can add the following companies in the landscape too:

– Nucleus Software in 2nd wave

– Greytip Software, Srishti Software in 3rd wave

– OrangeScape, Mettl and Kreeo in 4th wave.

Of course, there are many others but these are the ones that come to my mind the first.

May 30, 2014 at 3:29 pm

basicnext

Wish a tsunami of products from India!!